Calculating Car Loan Interest Rates

Calculate Car Loan Interest Rate: Your Ultimate Guide

Understanding how to calculate your car loan interest rate is crucial for making an informed financial decision. It empowers you to compare offers effectively, negotiate better terms, and ultimately save money over the life of your loan. This guide will walk you through the process, demystifying the calculations and providing you with the knowledge to secure the best possible car loan interest rate.

Many factors influence the interest rate you’ll be offered, including your credit score, the loan term, the vehicle’s age and price, and the lender’s policies. A higher credit score generally translates to a lower interest rate, as lenders view you as a lower risk. Conversely, a lower credit score may result in a higher rate to compensate for the increased risk. It’s also important to consider the loan term; longer terms often come with higher interest rates, although they result in lower monthly payments.

Understanding Simple vs. Amortizing Interest

Car loans typically use an amortizing interest calculation. This means that in the early stages of the loan, a larger portion of your payment goes towards interest, while a smaller portion reduces the principal. As you continue to make payments, the balance shifts, and more of your payment is applied to the principal. This is different from simple interest, where interest is calculated solely on the principal amount.

Amortizing interest allows borrowers to gradually build equity in their vehicle over time.

Key Factors Affecting Your Car Loan Interest Rate

Several elements play a significant role in determining the interest rate you’ll be offered. Lenders assess these factors to gauge the risk associated with lending you money. Understanding these components can help you prepare and improve your chances of securing a favorable rate.

Credit Score: The Biggest Influencer

Your credit score is arguably the most critical factor in determining your car loan interest rate. A higher score indicates a history of responsible credit management, making you a more attractive borrower. Scores are typically categorized, with excellent credit often yielding the lowest rates. It’s always a good idea to check your credit report before applying for a loan to identify any potential errors.

Loan Term and Amount

The duration of your loan, or loan term, also impacts the interest rate. Longer loan terms, while offering lower monthly payments, typically come with higher overall interest costs due to the extended period of borrowing. The loan amount itself can also be a factor, though typically less significant than your credit score.

Down Payment and Vehicle Age

A larger down payment can reduce the amount you need to finance, potentially leading to a lower interest rate. This is because you’re borrowing less, and the loan-to-value ratio is more favorable for the lender. The age and condition of the vehicle also matter; newer, more valuable cars may qualify for lower rates than older, used vehicles.

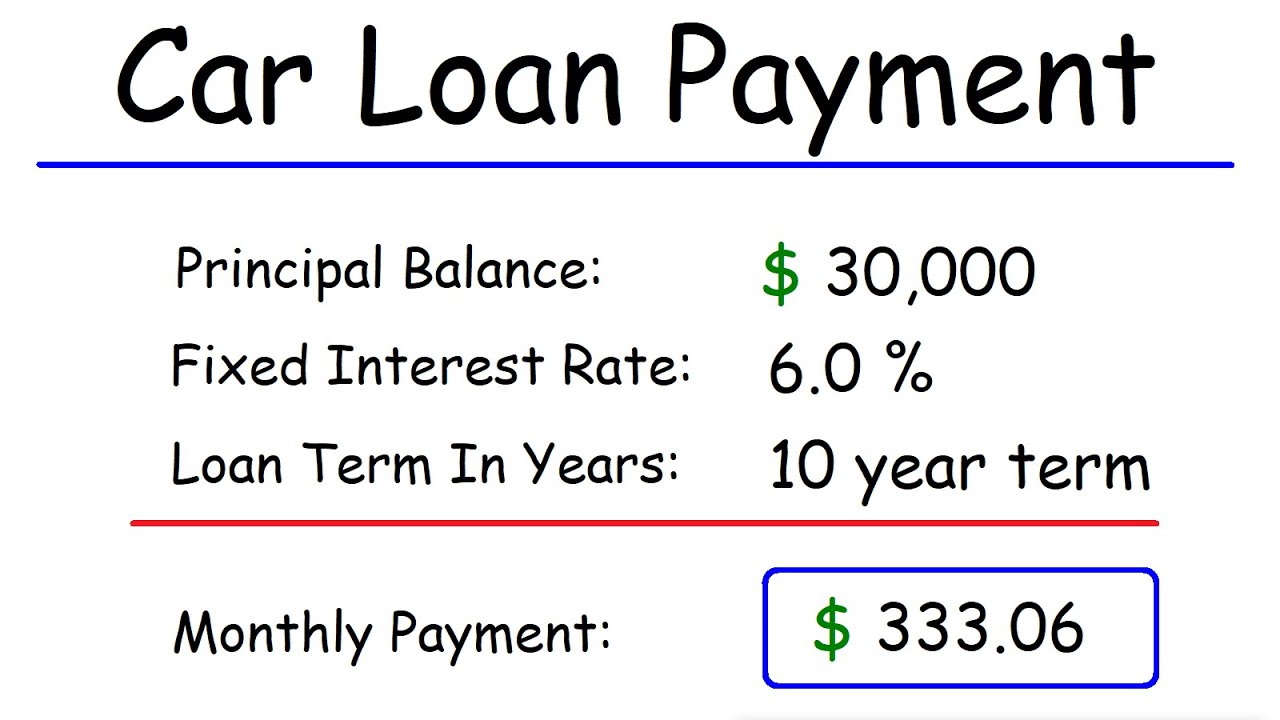

How to Calculate Your Car Loan Interest Rate

While lenders provide the Annual Percentage Rate (APR), understanding the underlying calculation can be helpful. The most common way to estimate your monthly payment and the interest you’ll pay is using an auto loan calculator. These calculators typically use the following formula:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (Annual Rate / 12)

- n = Total Number of Payments (Loan Term in Years * 12)

Example Calculation

Let’s say you want to calculate the monthly payment for a $20,000 car loan with a 5-year term and an 7% APR.

- P = $20,000

- Annual Interest Rate = 7% or 0.07

- i = 0.07 / 12 = 0.005833

- n = 5 years * 12 months/year = 60

Plugging these values into the formula:

M = 20000 [ 0.005833(1 + 0.005833)^60 ] / [ (1 + 0.005833)^60 – 1]

M ≈ $392.14

This calculation estimates your monthly payment, and by subtracting the principal from the total payments made, you can determine the total interest paid.

Tips for Securing the Best Car Loan Interest Rate

Negotiating a lower interest rate can save you a significant amount of money. Here are some actionable tips:

| Strategy | Description |

|---|---|

| Improve Your Credit Score | Pay bills on time, reduce existing debt, and avoid opening new credit accounts before applying. |

| Shop Around | Get pre-approved by multiple lenders (banks, credit unions, online lenders) to compare offers. |

| Negotiate Loan Terms | Don’t be afraid to negotiate the interest rate and loan term with the dealership or lender. |

| Consider a Co-signer | If you have a lower credit score, a co-signer with good credit can help you secure a better rate. |

Frequently Asked Questions (FAQ)

What is a good car loan interest rate in 2026?

Good rates can fluctuate based on economic conditions and your creditworthiness. Generally, rates below 5% are considered excellent for well-qualified borrowers. However, it’s essential to compare offers specific to your financial situation.

Can I refinance my car loan to get a lower interest rate?

Yes, if your credit has improved or market rates have dropped significantly since you took out your loan, you may be able to refinance your car loan to secure a lower interest rate and potentially save money.

How does a car dealership’s financing compare to a bank’s?

Dealerships often work with various lenders and may offer special financing deals. However, it’s always wise to get pre-approved by your bank or credit union first to have a benchmark for comparison and ensure you’re getting a competitive rate.

Conclusion

Effectively calculating and understanding your car loan interest rate is a cornerstone of smart car financing. By familiarizing yourself with the factors that influence rates, utilizing loan calculators, and actively shopping for the best deals, you can significantly reduce the overall cost of your vehicle purchase. Remember that a lower interest rate translates directly into more money saved over the loan’s duration. Take the time to research, compare, and negotiate to ensure you secure the most advantageous terms possible for your new car. Your financial future will thank you for it.